Is 2021 A Good Time To Buy Property In Malaysia? Here's All You Need To Know

Interest rates are at an all-time low, which means lower monthly instalments... for now.

By Jeremy Ng — 09 Jun 2021, 01:48 PM

If you're thinking of owning a property, but aren't sure whether it's a good time to buy now, don't worry! You've come to the right place.

Buying your dream home is one of the biggest purchases you'll ever make, so it's not something you should rush into. To help you make an informed decision, we'll be taking a look at three main things:

- Current property market trends

- How much you can actually afford

- Frequently asked questions by homebuyers

Current Property Market Trends

When considering whether to buy a home, it's important to understand the property market landscape – the idea is to buy low, sell high. While it may be difficult to predict exactly how the property market performs, there are a few trends in 2021 that interested homebuyers should keep an eye out for.

1. The government recently extended the Home Ownership Campaign (HOC) until the end of 2021

Recently, the Ministry of Finance has agreed to extend the HOC that began since 2019. Under this campaign, homebuyers can enjoy stamp duty exemption and 10% discounts on property.

For a RM500,000 home, that would mean up to RM61,250 in savings!

Plus, Bank Negara Malaysia has removed the 70% loan-to-value restriction on third home loans above RM600,000. This means if you're buying your third home, you can now apply for up to 90% financing.

What this means for homebuyers:

- You won't have to fork out a huge upfront sum to buy a home

- These savings are not applicable for sub-sale units

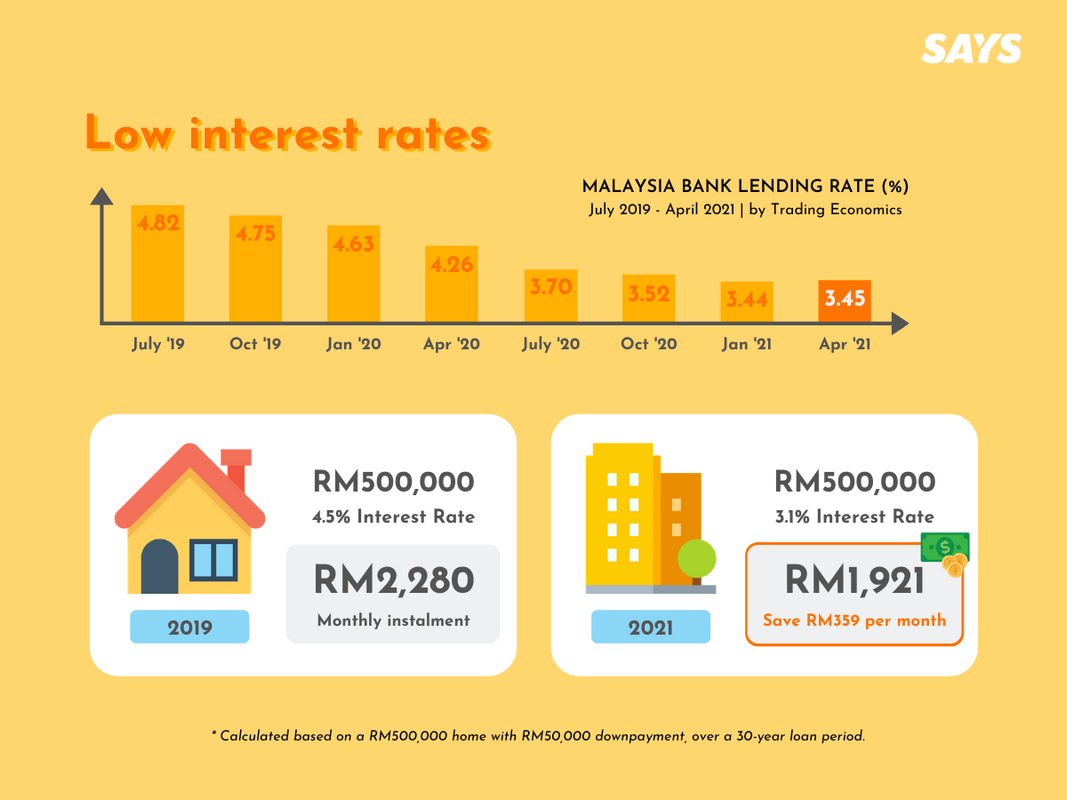

2. Interest rates are at an all-time low = lower monthly instalments

Bank Negara Malaysia's overnight policy rate (OPR) is at its lowest in two decades at 1.75%.

A low OPR rate leads to lower interest rates. In fact, a quick check on iMoney.my shows that banks are offering home loans with interest rates as low as 3.1%. Just two years ago in 2019, the average interest rate was around 4.5%.

To put things into perspective, for a RM500,000 house, you could save up to RM359 per month on your monthly instalments if you purchase a house right now. However, one important thing to note is that interest rates will gradually go back up as the OPR rate increases.

What this means for homebuyers:

- You'll be paying lower monthly instalments initially

- These monthly instalments may go up significantly, so don't overestimate what you can afford

3. Developers are offering never-before-seen deals

According to consultant firm Rahim & Co International, there were 57,390 units left unsold in Malaysia in Q3 of 2020. This could be because supply is higher than demand, or people just can't afford to buy a home.

That's also why developers are encouraging potential homebuyers to spend by giving amazing deals, ranging from free downpayment, free maintenance fees, free furnishing, to additional rebates.

Some developers are even offering 100% financing, which means you can own a home without any upfront costs; everything is included in your monthly instalments.

What this means for homebuyers:- You can potentially save a lot of money if you buy from developers

- The units available at a discount may be leftover units

So, to buy or not to buy?

With all the savings and attractive promotions, 2021 is a good year to buy a home. Nevertheless, as property investment is a long-term commitment, you must make sure you have the right financial backing and sufficient funds before deciding to buy a home.

Yes, you should consider buying a home if:

- You found a place that you genuinely love

- It is affordable for you, and you're financially secure

No, you should not consider buying a home if:

- You're looking to make a quick turnaround profit

- The only reason you're buying is because of the discounts

How Much You Can Actually Afford

One of the most important things when buying a home is sustainability. While a property's monthly instalment may seem affordable to you, would you still be able to maintain it down the road if you lose your job or have more financial obligations?

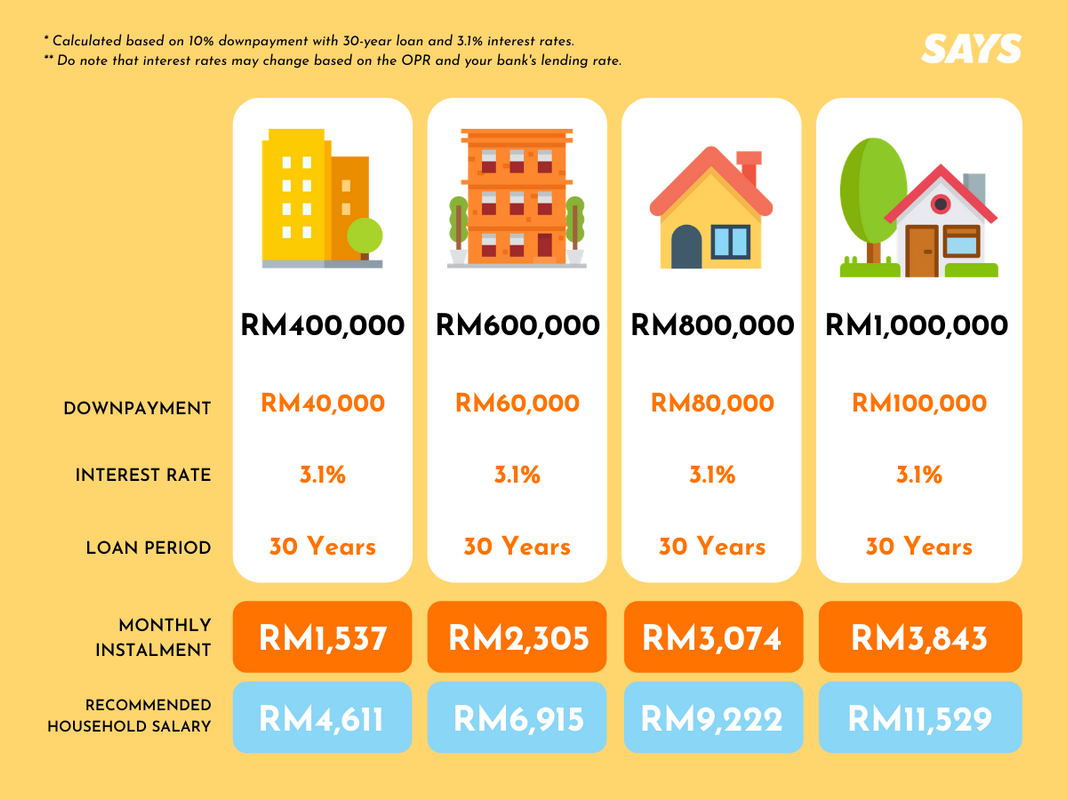

As a rule of thumb, iProperty.com.my suggests that your monthly loan repayment should not exceed one-third of your monthly income. However, what you can afford is also dependent on your other debt like car loans, credit cards, as well as monthly expenses.

For example, if you earn RM4,650 a month, you could possibly afford a RM400,000 home with a monthly repayment of RM1,537.

Wondering what kind of property you can afford? Check out this table below:

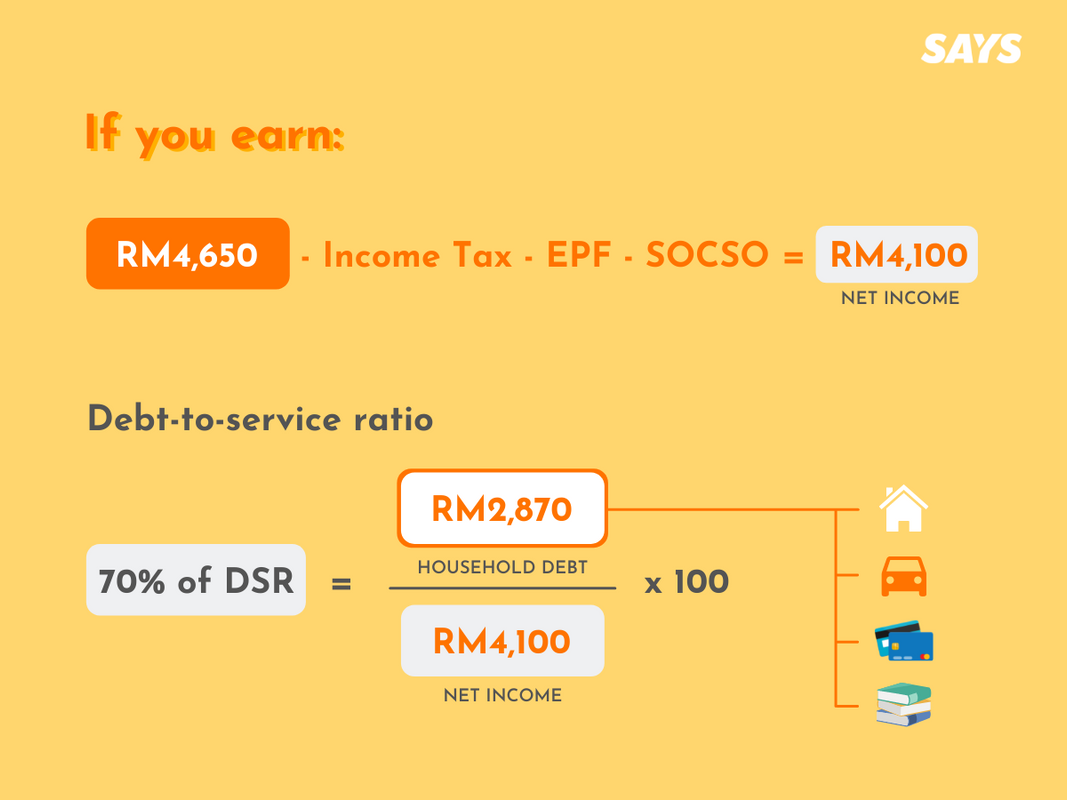

Another way to calculate how much you can afford is using your debt-to-service ratio (DSR), which should not exceed 70%. This formula is often used by banks to assess a homebuyer's loan eligibility.

DSR = Household Debt / Net Income x 100

For instance, if you earn RM4,650, you'll roughly have a net income of RM4,100 after income tax, EPF, and SOCSO deductions. To fulfil the 70% DSR rule, your household debt cannot be more than RM2,870 – this includes your home loan, car loan, credit card bills, and PTPTN loan.

Homebuyer FAQ

1. Is it better to buy a new launch property or a subsale property?

You may be able to find cheap subsale properties under market value this year. However, they come with additional upfront costs like legal fees, stamp duty, and renovation, some of which are waived for new launch properties.

2. Should I buy an under-construction or move-in ready unit?

If you're investing for the long-term, or want extra time to build your cash reserves, you can consider getting an under-construction home. Opt for a move-in ready unit if you're looking to stay in your new home soon.

3. What are important things to consider when buying a home?

Buy from a trusted developer

- With a trusted developer, you'll have better support and be less likely to run into problems in the future.

Buy for the future

- While you may not need a four-bedroom home now, your family size may grow in a couple of years, that's why you should get a home that will last.

Determine your priorities

- Everyone wants the best location, price, and amenities. However, you may need to sacrifice one for the other. Don't settle – be patient and you'll find the right home.

Know your budget

- The general rule is that your monthly instalments shouldn't be more than a third of your income.

4. How important is the location?

Very important! Look for homes within mature or up-and-coming townships, instead of homes in the middle of nowhere. Also, consider the surrounding amenities, and how easy it is to get around – some homes may be further away, but still well-connected.

5. Freehold and leasehold, what's the difference?

Freehold homes are fully owned by the homebuyer, while leasehold homes are owned by the government and have a tenure of 30, 60, 99, or 999 years. While freehold homes are more desirable, leasehold homes tend to be cheaper and offer better facilities.

If you're buying a home to stay, land tenure shouldn't be your sole deciding factor – instead, choose a place that you'll be happy to live in.